Massimo Garbuio

Intangible assets: undervalued and under rewarded by local investors

Since it went public in 2015, Atlassian, the software company Australia is proud to call its own, but which is listed in the US, has increased its share price by 1,100%.

Gelion, a company that aims to revolutionise battery technology based on research undertaken at the University of Sydney, listed on the London Stock Exchange in December last year.

Why would two innovative Australian companies with compelling investor inspiring narratives to pitch, choose to take their share offerings offshore?

Could it be these companies – with their offerings heavily weighted towards intangible assets (IA) – realised the Australian investor market would not fully appreciate – and properly price – what they had to offer?

Intangible assets – say my name

Intangible assets are assets that are not physical in nature. Goodwill, brand recognition, intellectual property (such as patents, trademarks and copyright) data, even software are all intangible assets.

While many investors clearly find it difficult to come to grips with the real worth of a company’s IA – recent research has shown that companies also don’t understand what assets they own. Unfortunately under current accounting standards, IA are often ignored – they are either off balance sheet or lost under the amorphous term ‘good will’.

So if companies are not adequately capturing their real value – how can we expect investors to appreciate the worth and the long term potential of these assets?

Losing both ways

It all adds up to Australian companies missing out on local capital that could further power their growth. And Australian investors are missing out on the returns these assets are absolutely generating.

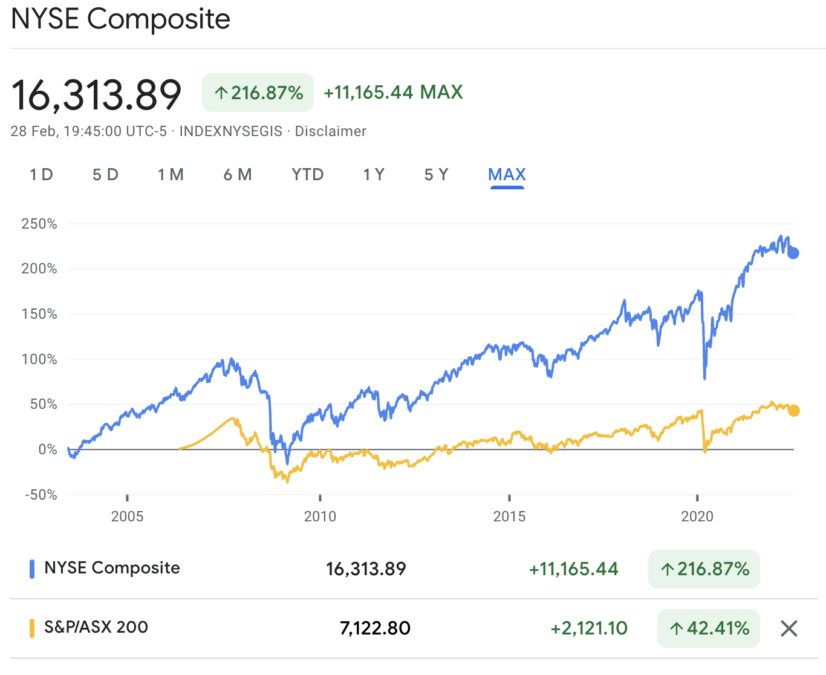

The ASX has underperformed the US markets since the global financial crisis, especially in the last financial year.

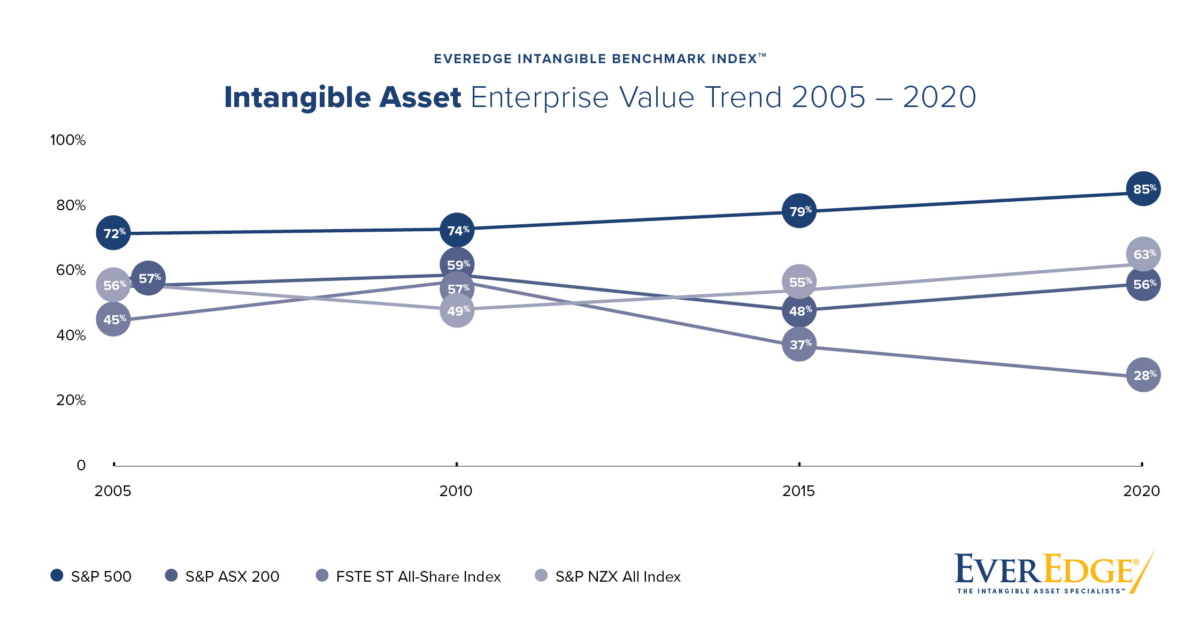

Recent research by EverEdge has highlighted that, whereas in the last ten years intangible assets as a percentage of enterprise value has steadily increased, that growth has been much more pronounced in the S&P500 than in the ASX. US markets recognise that most value nowadays is due to intangible rather than tangible assets and reward those companies that invest in intangibles even more – tech stocks being at the forefront of that growth.

Today, intangible assets are the primary drivers of company value. These assets account for more than 90% of all company value and drive virtually all earnings and profit growth, whereas 40 years ago this figure was barely 17%.

US markets reap IA gains

It all adds up to the fact that investors would have been better off investing in US shares than Australian shares over the last 24 years. Since the global financial crisis the Australian Stock Exchange has underperformed compared with the NY Stock Exchange.

We need to change both how we look at and value investments or the best companies will list overseas and not on the ASX.

Blinkered thinking by executives and investors

There are two fundamental differences between the Australian and the US investment market:

- Australian executives seem to think they do not need to deploy speculative capital (that’s the capital that goes into developing innovation and intangible assets). These assets take longer to provide returns to investment, are riskier but ultimately provide greater growth. If your domestic market is fundamentally protected from outside competition, why would you need to ‘risk’ capital on innovation, intangible assets and growth?

- Australian shareholders, whether mom-and-pop investors looking for dividends and retirement, or larger pension funds, expect stable and predictable returns. They don’t like surprises. If investors expect this, then executives follow through by investing in non-risky assets.

Big picture thinking

There are wonderful exceptions to the above two points. Cochlear and more recently, to some extent, Afterpay have been able to change the story of what a company is going to deliver: growth over time rather than dividends. These companies seized control of their own narratives and convinced shareholders to go on the investment journey with them. This gave both organisations breathing space to forget about quarterly expectations and dividends, freeing them up to focus on deploying capital on the truly more rewarding initiatives they had to offer.

New breed of investor

A new type of retail investor has emerged from the COVID-19 pandemic. Labelled the ‘Generation Investors’ they are younger and willing to invest for the longer term. Will they be the force that change companies’ narratives and especially executive attitude towards innovation, risk and building great intangible asset bases?

Dr Massimo Garbuio is an Associate Professor in Entrepreneurship at the University of Sydney. He's passionate about helping students and business leaders become master strategists.