The rise of the value destroyers – activist short sellers

When several activist hedge funds announced their short positions in Tesla’s stock, its CEO, Elon Musk, accused them of fabricating rumours, calling them “value destroyers” who distracted the company from long-term value creation and key innovation activities.

A new type of short selling has emerged, with huge ramifications. Short selling is a controversial practice where traders borrow securities and sell them in the hope of then buying the stock at a lower price in the future.

Typically, short sellers keep their ‘short’ position secret, but this has changed in recent years. Enter the activist short seller: after opening a short position on a stock, the aggressive short seller publicly denounces their target by making allegations, such as accounting irregularities and product deficiencies, or merely alleging the stock is overvalued. In this way they can further drive the target stock’s prices down to achieve higher profits.

The GameStop short squeeze, in 2021, shows that activist short sellers have become villains in the eyes of retail traders. Critics, and particularly management targeted by activist short selling, have accused these traders of manipulating markets, spreading falsehoods, and causing target companies long-term economic damage.

The damage inflicted by some activist short sellers is more ‘visible’ than others. When Kyle Bass, head of Hayman Capital Management, legally challenged 37 patents filed by firms he targeted, some firms experienced real value declines. While only 7 of the patent challenges succeeded, Bass’s public short campaigns caused anxiety among pharmaceuticals investors when they were launched.

Do activist short sellers actively destroy the value of firm investments in addition to their role in ‘correcting mispricing / overvaluation’? Suppose a firm’s ‘true’ stock value is $20 and it was indeed overvalued and traded at $30 before the public short campaign: will activist short sellers’ public attacks (e.g., legal challenges toward patents) actively reduce the stock’s fundamental to, say, $15? If so, an activist short seller’s potential trading profit can increase from $10 (price decline from $30 to $20) to a bigger gain of $15 (price decline from $30 to $15), where the $5 trading profit is due to the campaign’s negative real impact on target stocks (fundamental decline from $20 to $15).

In a recent study, we examined whether activist short selling negatively affects key corporate innovation activities, using a novel dataset of new product and service announcements from Capital IQ’s Key Developments database.

We found that activist short selling substantially reduces their targets’ new product introductions (NPI) even after accounting for the possibly superior stock-picking abilities of activist short sellers.

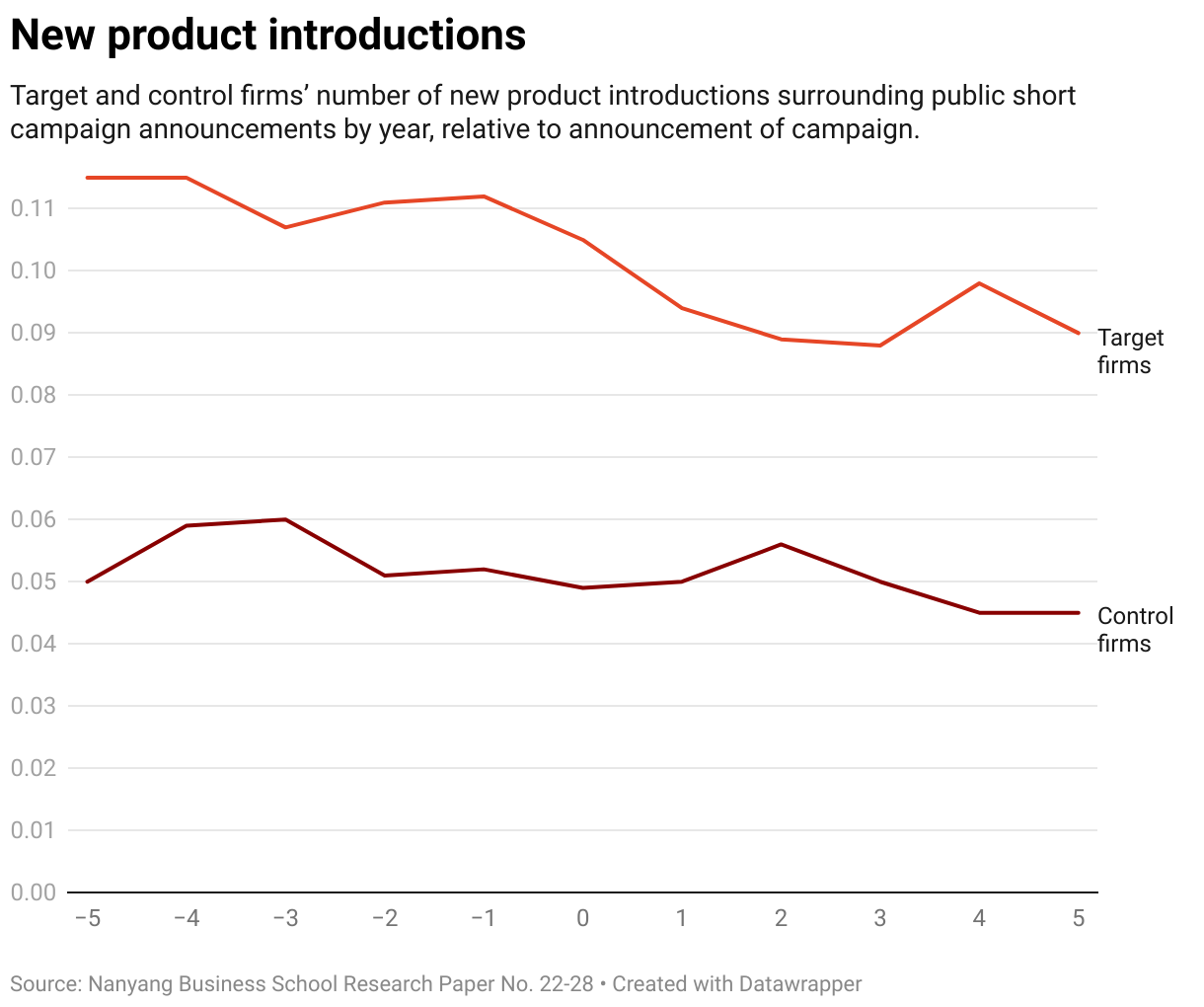

We looked at 274 activist short campaigns announced over the period 2010-2017 targeting firms headquartered in the United States: Figure 1 demonstrates that target firms experience greater declines in the NPI per year relative to control firms for up to five years following activist short selling announcements. Further, relative to their matched control firms, activist short selling target firms introduce 11.2% fewer new products per year, on average, after being targeted. The negative impact of activist short selling lasts up to five years after the campaign announcement, indicating that the product market impact is not transitory. Furthermore, target firms experience long-term decreases in innovation productivity as well as product quality.

As in the Kyle Bass incident, we found the decline in product innovation is partly due to key stakeholders withdrawing their support from the target firm. The negative publicity adversely affects stakeholders’ perceptions of the target firm’s future products. We found the negative product impact of activist short selling is especially prominent among firms most vulnerable to declining support from three types of stakeholders: capital providers, customers and employees.

After being targeted, firms reduce the capital they raise and have worse relationships with their customers. Shareholder support for key management proposals in annual meetings also declines, and sales to major customers fall significantly, relative to control firms. We also found that rival firms of targets benefit through increased product output.

We were able to rule out several alternative explanations. Target firms’ product problems cannot be explained by management making myopic cuts to innovation investments to boost short-term performance in defence against activist short campaigns. Moreover, we carefully account for the selection issue where activist short sellers may be able to detect target firms with future product innovation problems that are unobservable to the general market. Using Heckman’s two-step selection model and a strong instrumental variable, we find that target firms continue to have trouble with their products. Thus, while selection might partially drive the results, it cannot be the sole reason.

Our paper has several important implications. We show that the public nature of campaigns launched by activist short sellers has an incremental and distinct impact on firm activities through their broader influence on key stakeholders. This contradicts the findings of other papers that traditional short selling can improve corporate performance through disciplining managers.

We also disprove the notion that financial markets are a mere sideshow to the ‘real’ world of corporate activities. Or to put it in positive terms – information from the financial markets does affect the allocation of firm investments. We provide empirical evidence of the stock market’s feedback effect on firms’ decisions by showing that their non-financial stakeholders also learn from financial markets, including customers and employees.

While activist short sellers’ claims are often creditable, their public attacks can further worsen the target’s existing problem and the stock’s fundamental value, causing additional damages to the target firm.

There are now moves to regulate activist short sellers. In 2022, the U.S. Securities and Exchange Commission (SEC) published and requested comment on a proposed new rule on short selling, which aims to promote greater transparency of short selling activities and mitigate the risk of activist short sellers illegally manipulating stock prices.

Our paper highlights the importance of considering the cost of activist short selling even if we assume their allegations and intentions are creditable: due to the stock market’s feedback effect, public short attacks may harm target firms by worsening their existing fundamentals. Moreover, the negative product impacts of activist short selling we document contrast with previous findings that traditional short selling can improve corporate performance. It is important for regulators and the market to distinguish between activist short selling and traditional ‘silent’ short selling when considering new short selling disclosure rules.

Claire Liu (University of Sydney), Angie Low (Nanyang Technological University), and Talis Putnins (University of Technology Sydney) recently published a paper entitled, “Spiraling Downward: The Real Impacts of Public Short Campaigns on Product Innovation”.

Image: lo lo

Dr Claire Liu is a Senior Lecturer in the Discipline of Finance at the University of Sydney Business School. Claire’s research interests are in the broad area of empirical corporate finance.