SDGs by 2030 – are we on track?

Clean and secure water for everyone – an accounting story

India, which has 18 percent of the world’s population but only 4 percent of the world’s water resources, will become water scarce by 2025. India is highly dependent on limited fresh water sources, including the annual Himalayan melt.

Conversely in Australia, water supplies are dependent on unreliable rainfalls, and for many, on what lies beneath: the Great Artesian Basin, one of the world’s largest underground freshwater reservoirs.

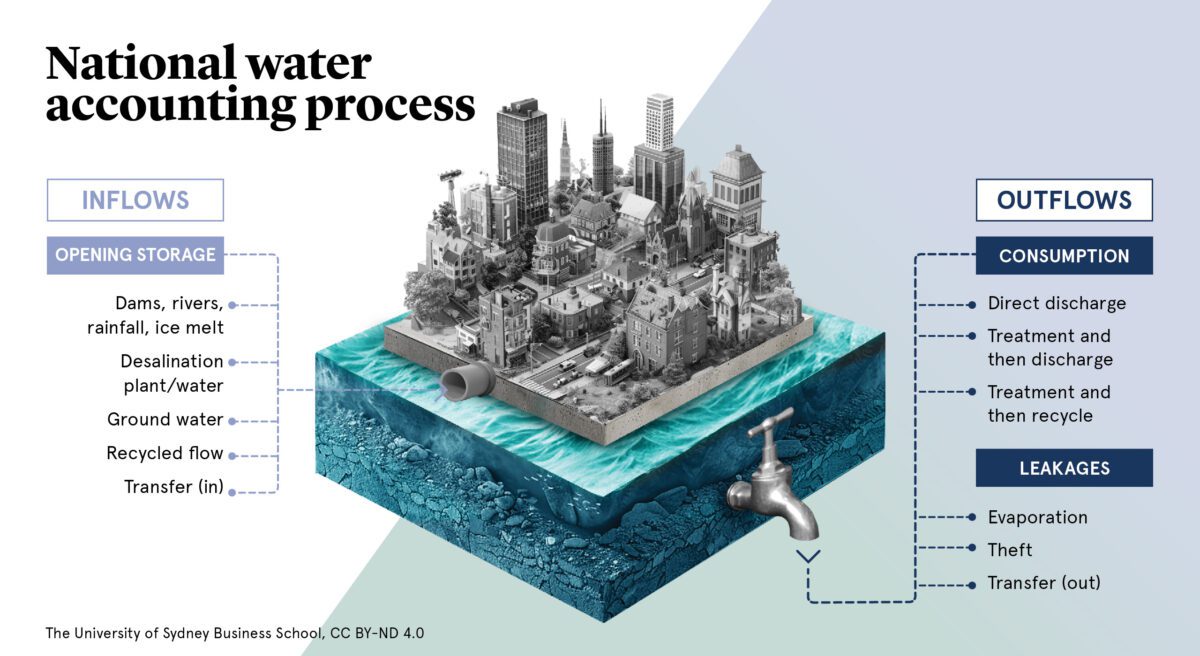

Effective water supply management requires attention not only to geography and the weather. To achieve SDG 6, nations need to be able to answer a number of accounting questions:

- How much water is available?

- What volumes of water are used, and for what purposes?

- How is it being replenished?

- Can it be transferred?

- Where are the leakages?

- Where is maintenance required?

- Where are the corruptions in the system?

- Where is the pollution that is spoiling water supply?

- What happens to the outflows?

Unlike a lot of other ‘sustainability’ related challenges, water lends itself to accounting quite well, because it is relatively easy to conceive of resource flows in and out, and of balances at the end of reporting periods. Accounting principles can therefore contribute to addressing these questions, and by extension, to achieving SDG 6.

India and Australia demonstrate that a nation’s disparate water supply challenges are highly idiosyncratic, depending on geographically bounded considerations. Each nation must adopt a tailored approach to account for its total water supply, as the appropriate responses vary widely. Therefore, every country requires a customised national water accounting method to effectively address these issues.

Infrastructure may be the key challenge for some countries. For example, in India, where 54 percent of households lack access to safe sanitation facilities, the government is responding with a range of projects, including attempting to improve household water security by installing taps into every home. Alternatively, differing approaches to water accounting in Libya could have revealed the poor quality of two major dams (national assets) which collapsed in 2023, killing more than 11,000 people.

No one knows how much water Australia’s Great Artesian Basin holds. Nor how it gets replenished on a circular basis. Effective water management demands a better understanding of (and accounting for) such unknowns.

Efficiency and risk are additional important elements of any effective water accounting process.

Efficiency issues require insight into the total quantities of potable water available, and then consideration of the diverse needs of different consumer groups (households, businesses, etc,) along with the nation’s ecological needs.

Risk, particularly in relation to climate change, is a significant further complication. The accounting challenge is no longer simply identifying the supply that’s available every year. We also need to factor in the greater uncertainties about supplies in future years. Accounting for water is becoming increasingly difficult.

In short, every country needs to think about how it can support targets 6.4 ,6.5 and 6.6, via improved water accounting information. Despite differing challenges, the most important water management mechanism is clear direction and action from authorities. Strong regulatory underpinnings are needed to support targets. Effective and bespoke accounting solutions then emerge as critical tools to support that journey.

Sustainable Development Goal (SDG) targets addressed:

Target 6.3 By 2030, improve water quality by reducing pollution, eliminating dumping and minimizing release of hazardous chemicals and materials, halving the proportion of untreated wastewater and substantially increasing recycling and safe reuse globally.

Target 6.4 By 2030, substantially increase water-use efficiency across all sectors and ensure sustainable withdrawals and supply of freshwater to address water scarcity and substantially reduce the number of people suffering from water scarcity.

Target 6.5 By 2030, implement integrated water resources management at all levels, including through transboundary cooperation as appropriate.

Resources

How would you develop a water accounting tool kit?

Consider three different countries: what are their respective water challenges? What do you see as the important steps that could be taken to ensure a more secure water supply?

What are the most pressing challenges for the water supply in (Country X)?

What are the key metrics that would need to be included when constructing a national water account for that country?

Book

- Egan M and Agyemang G (2022) An exploration of developing approaches to water accounting. In: Handbook of Accounting and Sustainability. Edward Elgar Publishing; 279-299

Websites

Dr Matthew Egan is a Senior Lecturer in the Discipline of Accounting at the University of Sydney Business School. His research interests focus primarily on sustainability, and how accounting can contribute to addressing related questions.